Page updated

HM Treasury’s Asset Management Taskforce was set up in October 2017, with an overarching objective to maintain a thriving UK asset management industry. As part of its commitment to help the Taskforce achieve its objectives, the IA established the UK Funds Regime Working Group (UKFRWG), comprised of senior figures from the asset management industry, as well as Government, the FCA and the Financial Services Consumer Panel.

Image

The Group submitted a report to the Taskforce in June 2019 which offers a set of concrete proposals to government and regulators on how to retain and improve on UK fund industry competitiveness, from both a domestic delivery and international customer perspective. While all of the proposals would be relevant even without Brexit, Brexit gives the questions – and recommendations - an additional importance.

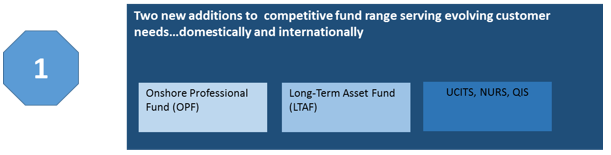

The Report makes clear that the future of UK competitiveness relies on the sum of many parts rather than tackling issues individually. It sets out a blueprint with specific actions in three thematic areas, including two significant additions to the UK fund range: a new Onshore Professional Fund regime and a Long-Term Asset Fund (LTAF)

During 2020, the IA produced a new paper on the LTAF and a summary sets out the key elements.

Facilitating Innovation

While innovation can often take place without the need for specific policy, regulatory or tax changes, some areas require greater facilitation. Reflecting current and anticipated future needs of customers in the UK and internationally, the UKFRWG put forward specific proposals for two new fund structures that will help to ensure the industry can deliver effectively:

- A UK Long-Term Asset Fund (LTAF) to help certain groups of customers, particularly in the DC pensions and parts of the retail market, access private markets effectively.

- A new type of alternative UK investment fund that is attractive to professional investors, titled the Onshore Professional Fund. This would be distinct from the Qualified Investor Scheme (QIS) and require corporate and contractual vehicles as well as a substantially enhanced partnership structure.

Detailed work on the retirement income market by the Group suggests that there is scope to facilitate further innovation in the drawdown market with changes to the way in which income and capital are treated within funds, thereby allowing a more targeted approach to the delivery of sustainable income throughout retirement.

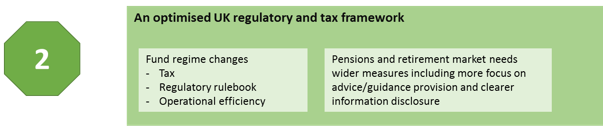

Optimising the existing regime

The Report identified a number of areas where enhancements can be made:

- Building on improvements in the UK tax environment for UK domiciled funds in recent years, the Report addressed residual areas of tax drag in UK authorised funds and recommends a full review (being undertaken through 2020-21) of the fund tax regime as well as measures with respect to withholding taxes and access to tax treaties and changes to the UK VAT regime.

- The Report recommended the creation of a single rulebook for funds as well as repackaging NURS fund structures and its subsets as a ‘UCITS plus regime’ and explores the benefits of master-feeder structures as a gateway to open up funds in other jurisdictions.

- The Report made recommendations for an optional alternative investor dealing model to the traditional model operating in the UK today. This ‘Direct2Fund’ model would facilitate investors transacting directly with the funds and remove the Authorised Fund Manager (AFM) as a counterparty to the investor deal.

While the Report concludes that UK authorised funds are already capable of meeting the needs of retirement customers to a significant extent, the Report identified a range of enhancements to help pension schemes and retirement investors benefit from more efficient investment strategies. These include minimising tax leakage in investment funds, enhanced flexibility around distribution of capital as income to allow for innovation in retirement-focused funds and progress of the LTAF in conjunction with amended permitted links rules for life funds.

Support and promotion

Success of improving the competitiveness of the UK fund regime is also conditional on two crucial additional elements outlined in the Report:

- A commitment to promotion: government and regulators should work with the industry to promote the UK specifically as a fund management centre, helping to cement the UK’s place as a leading global hub for investment management.

- A framework for ongoing dialogue is needed between asset managers, policymakers and regulators. This could take the form of an ‘Investment Management Forum’ which would bring together key participants, including HMT, the FCA and the IA and other industry bodies with an interest in fund regulation.

HM Treasury Review of the UK Funds Regime: A Call for Input

In January 2021, HM Treasury issued a Call for Input into the UK Funds Regime. The Call for Input built on the work of the UKFRWG, along with other industry proposals and discussed changes to the UK funds regime covering three areas:

- The UK's approach to fund taxation

- The UK's approach to fund regulation

- Opportunities for wider reform

The IA issued a circular, which explores the details of the paper.

The IA responded to the Call for Input in April 2021. The response can be found here.

Direct2Fund

D2F originally formed a part of the UKFR work, and is the proposal to produce an optional alternative dealing model for UK funds, removing the AFM from the deal and thereby eliminating counterparty risk and increasing the attractiveness of the UK as a fund domicile.

More detail on the proposals, and recent activity can be found here.

FCA Discussion Paper 23/2: Updating and improving the UK regime for asset management

In 2023 the FCA published a Discussion Paper asking for views on changes to the UK asset management regime to advance the UK competitiveness agenda.

In the DP, the FCA stated that it is considering a wide range of ideas, including how it can support firms’ use of technology to improve customer experience and efficiency. The paper also discussed how the FCA’s rules could be streamlined and improved to help firms deliver better support to investors, retail and wholesale, UK-based and international.

The discussion paper was in four parts:

- Chapter 3: The structure of the regulatory regime for asset managers, as originally derived from EU directives. It covers the framework of rules for asset managers, the regime for retail funds and the regime for managers of professional funds.

- Chapter 4: FCA's thoughts on how they could improve the regime for asset management and funds. It mainly covers possible changes to the rules relating to fund managers, depositaries and funds, such as the responsibilities of host AFMs and enhancing liquidity management.

- Chapter 5: FCA's thinking on the role of technology in supporting better outcomes from authorised funds. Includes D2F, fund tokenisation, investments in tokenised assets and cryptoassets.

- Chapter 6: considers how the fund rules could be revised, in the light of developments in technology, to improve investor engagement with documents and output such as the fund prospectus, the report & accounts and the requirements around unitholder meetings such as EGMs.

The IA's response to the Discussion Paper can be found here.